You purchased a private condominium or HDB flat?You have signed up with bank for fixed or floating rate 2 or 3 yrs back?Tips for not paying higher interest ratesThen its time to read the Terms and conditions of the bank and recall the claw back period. Usually, banks will have 2 yr locking rate and the third year will have higher rates being quoted. If customers forget to track the loan tenure then they end up paying high interest rates.How to avoid paying higher interest rates?Usually customers need to serve 3 months notice for bank if they need to switch to another bank and hence it is adviced to start doing market survey on the new interest rates offered by other banks 4 months before the full redemption date.What is redemption date?It is the date mentioned in your contract after which the refinance or switch to other banks is possible without any penalties.What is the best way to do market survey?Register with aggregators such as few mentioned below and speak to mortgage advisors who will give you the current rates offered by bank with some promotions if any

- Redbrick

- Mortgagewise

- Icompareloan

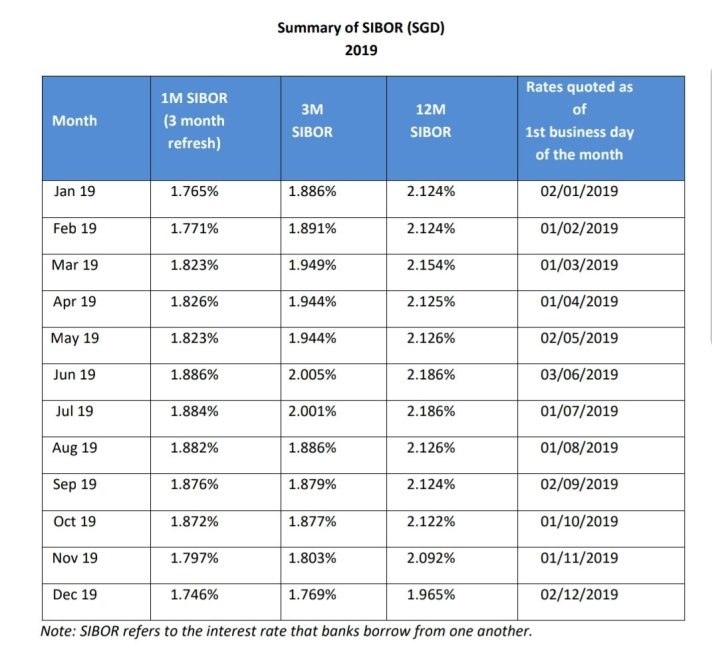

How to decide if fixed or floating rates to be choosed?In the year 2012, banks were offering sibor rates which were very low at that point of time. In the year 2019 banks are offering fixed price which is comparatively lesser than the floating rates.As a consumer, do you need to opt what majority banks offer?Not necessary, in the year 2012 i opted for fixed(1.35, 1.68, 1.58) because i anticipated that the floating rates will slowly rise and it did.In the year 2019 i signed up for floating(1.87 + 0.20 spread value) keeping in view of the US fed rates slowly being cut due to economic slow down and US-China trade war.

This is a calculative risk i am willing to take. So before you decide to go against the wave pls do a thorough study and have some extra cash to settle the EMI incase if it rises.Useful Linkshttps://abs.org.sg/rates-siborhttps://youtu.be/4GonTct2WMk